- Build the Future

- Posts

- Nickel and Tech

Nickel and Tech

Every electric car manufacturer in the world needs nickel, and it plays an integral part in the car supply chain.

Mark Stevenson

August 02, 2024

Market capitalisation is a pretty poor metric for investors to use. What investors and business owners should care about is free cash flow, which is the cash available at the end of the day for distribution to shareholders. Having said that, today we will use market capitalisation for something, and that something is to compare the largest companies over time.

As I write this today, the largest public companies are:

Company | Country | Sector | Market Capitalisation |

|---|---|---|---|

Microsoft | United States | Technology - Software and Hardware | $3.3 trillion |

Apple | United States | Technology- Software and Hardware | $3.2 trillion |

United States | Technology - Semiconductors | $3.2 trillion | |

United States | Technology - Software and Hardware | $2.2 trillion | |

Amazon | United States | Technology - Software and Retail | $2.0 trillion |

Meta | United States | Technology - Social Media | $1.3 trillion |

Taiwan | Technology - Semiconductors | $0.9 trillion | |

Berkshire Hathaway | United States | Conglomerate | $0.9 trillion |

Eli Lilly | United States | Pharma | $0.8 trillion |

United States | Technology - Semiconductors and Infrastructure | $0.7 trillion |

Two things are noticeable about this list. The pre-eminence of American companies and the pre-eminence of technology companies. The last fifteen years have seen one of the greatest economic performances in history. The American technology industry, mainly centered in Silicon Valley, has upended markets, produced new products and achieved global dominance within the sector, underpinned by strong business models, rapid expansion and technological innovation. It’s also made more than a few people very wealthy and it’s made quite a lot of people quite wealthy. The tech dominated Nasdaq has a 15 year return (2009 - 2024) of 873% (16.4% annually), compared to the S&P returning 495% (12.6% annually), and the Dow Jones Industrial Average returning 362% (10.7%). In 2023, American companies accounted for 32 of the 50 largest publicly traded firms by market capitalisation.

Impressively, Microsoft and Apple were both formed in the mid-1970s and are still market and world leading companies today, despite the founders not leading their companies for well over a decade. Microsoft, in particular, pioneered the software industry before most people knew what software was.

However, this has led to the most concentrated S&P500 we’ve seen in decades. The ten largest US stocks account for about a third of the index, above the concentration levels of the dot-com bust. In 1995, the market cap of the world’s top 50 firms was about 9% of global GDP, in 2023 it was 27%.

Immensely large companies exist outside of public markets (although there a fewer): ByteDance is valued at about $250 billion, SpaceX is around $200 billion, Stipe is at $95 billion, OpenAI is at $80 billion, and Ant Group is also at about $80 billion.

However, the challenge for any investor isn’t so much understanding what is happening now (even though that’s a big enough challenge on its own) but forecasting which companies will be successful in the future, five years from now, ten years from now and twenty years from now. In a world of quick change, identifying those business models and companies that have a durable competitive advantage is hard but will be lucrative.

To indicate how much things may change, let’s take a look at the public markets in 2006, before the financial crisis. In 2006 the largest companies by market capitalisation were:

Company | Country | Sector | Market Capitalisation |

|---|---|---|---|

ExxonMobil | United States | Oil & Gas | $0.47 trillion |

General Electric | United States | Conglomerate | $0.38 trillion |

Microsoft | United States | Technology - Software and Hardware | $0.29 trillion |

Citigroup | United States | Financial Services | $0.27 trillion |

Gazprom | Russia | Oil & Gas | $0.27 trillion |

Industrial and Commercial Bank of China | China | Financial Services | $0.25 trillion |

Toyota | Japan | Automotive | $0.24 trillion |

Bank of America | United States | Financial Services | $0.24 trillion |

Royal Dutch Shell | Netherlands / United Kingdom | Oil & Gas | $0.23 trillion |

BP | United Kingdom | Oil & Gas | $0.22 trillion |

Figures not adjusted for inflation.

In 2006, we saw more diversity across countries and sectors: Financial Services and Oil & Gas are the primary industries represented. China Mobile, HSBC, AT&T, Walmart, Sinopec, Pfizer, PetroChina, Procter & Gamble and Petrobras were also large companies just outside the top ten. The only company that has maintained its level as one of the highest valued publicly traded companies is Microsoft.

In the private sector, Klarna is a cautionary tale. At the peak of its valuation in 2021, Klarna was valued at $45.6 billion. A year later, in 2022, it was valued at $6.7 billion, and the valuation has got nowhere near the previous high of $45.6 billion. Venture capital backed startup valuations can become disconnected from the fundamentals. Ant Group, still one of the most valuable private companies in the world, was valued at over $300 billion during a planned 2020 IPO.

But the challenge with market capitalisation, and why it is a poor metric, is that it’s based on current market expectations. The price, though often a good indicator of value, is often not. This is why value investors exist and why a very small number of people can beat the market. As Benjamin Graham wrote: “Mr. Market is there to serve you, not to guide you.” In other words, you develop your own valuation and then compare it to the stock price. You don’t use the price to determine your value.

Technology dominates our first list of the most valuable companies in the world, but it didn’t always, and it won’t always. The long boom in the technology sector permeates far and wide throughout our economy. As demand for GPUs has skyrocketed in the age of artificial intelligence, Nvidia’s valuation has risen. There’ll be other winners too.

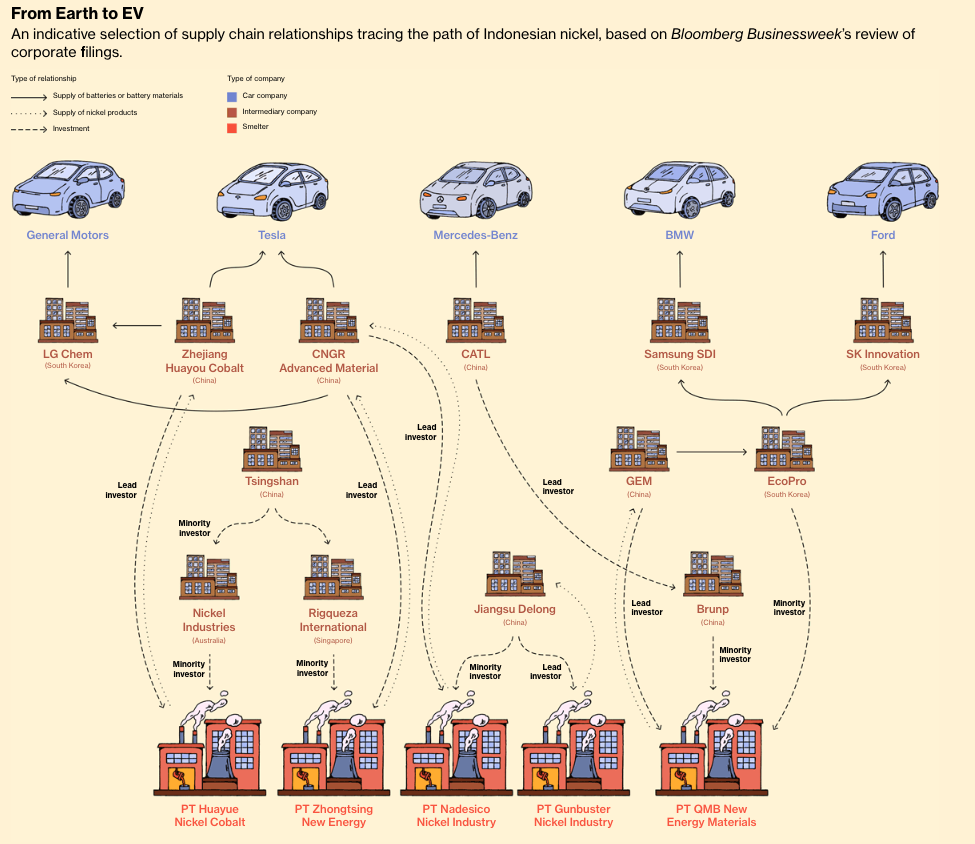

The nickel mining sector has seen and will see plenty of investment. Nickel-rich cathodes have a higher energy density in electric vehicle batteries, which allows EVs to store more energy and, therefore, have a larger range. Every electric car manufacturer in the world needs nickel, and it plays an integral part in the car supply chain.

As demand for nickel has soared, investment in mining to extract nickel, process it, and supply more processed nickel to the market has increased, driving down the price.

Indonesia has the world’s largest reserves of nickel and is the world’s largest exporter. The country has seen investment flow into the country to extract mine nickel. Most of the investment has been from China which has been ahead of the game at realising the strategic potential of nickel. China invested $3 billion into the nickel mining sector in Indonesia in Q4 2022. Indonesia is using its natural resources as an opportunity to build an electric vehicle ecosystem. It has offered tax breaks to investments in nickel and EV related industries. They banned exports of unprocessed nickel and now only export processed nickel. Indonesia’s global share of processed nickel has risen to ~50%, with forecasts that it could rise to somewhere around 60 - 75%.

This is a clear change in Indonesia’s economic policy and development. It has moved from extracting and exporting raw commodities to processed commodity exports, therefore adding value within the supply chain.

In July 2024, two South Korean companies, Hyundai and LG Energy, opened a $1.1 billion battery cell plant in Indonesia. Indonesia has been able to achieve solid 5% GDP growth rates (with the exception of the Covid hit years of 2020 and 2021), partially due to its embrace of nickel mining. The ecosystem development offers opportunities for local Indonesian firms to expand and to vertically integrate.

Of course, this macroeconomic industrial shift will likely lead to the growth of Indonesian mining companies such as PT Value Indonesia. But Chinese companies such as Tsingshan Holdings Group, which has been operating within the nickel industry in Indonesia since 2009, will also benefit.

Nickel and the EV industry provide the means for the Indonesian economy to grow. Though economic development will be led by private capital and private firms, the wider macroeconomy will benefit. But for business investors, it is the impact of individual companies and their ability to build a competitive durable advantage that delivers investment returns. The creation and growth of companies, if successful enough, provide the foundational building blocks for an entire ecosystem, which benefits from the economic tailwinds for decades afterwards.

Nickel mining is an increasingly large and strategically important industry. However, it has one major disadvantage that the technology industry does not have: It will face the common challenges of a commodity industry (price volatility, supply chain disruptions, a high regulatory environment, operational risks, and capital intensity). There’s a second challenge, too: the growth of nickel mining has been driven by the demand for batteries in EVs, and the car industry is notoriously volatile and challenging.

Reply