- Build the Future

- Posts

- Risky (Averse) Business

Risky (Averse) Business

The past is a good measure of the laws of physics. The past is a good measure of the laws of economics. But the past is a poor measure of risk.

Mark Stevenson

August 30, 2024

Whenever you invest or make any business decision, you take some risk. It’s risky business. However, when we think of risk, we often think of risk as being synonymous with volatility. If the price of an asset has greater price volatility, it’s considered riskier than an asset with less historical volatility, which seems silly.

This is a really deficient way to think about risk. It’s no surprise that the great investors, like Howard Marks and Charlie Munger, don’t equate volatility with risk. Instead, they see risk as the probability of losing money.

And I agree.

Large businesses, especially financial services companies, employ many thousands of people in large risk functions to measure every possible risk: business, credit, price, and operational risks. For the benefit of all of us, they probably should. In banking, if you get things wrong, there is no way back. Lehman Brothers, Long Term Capital Management, Silicon Valley Bank and Credit Suisse are all on the banking scrap heap.

I’m a believer in quantification. However, the existing ways to measure risk, with tools such as Value at Risk (VaR), give a false sense of security. In particular, VaR is very bad at predicting extreme, once in century conditions, for the simple reason that the training data for these models would never have seen these conditions before. There have been some changes in the last couple of decades - the assumption of a normal distribution of returns has gone out of the window, and the fat tails of the curve are now fatter. It’s an acknowledgement that rare events are … not that rare.

Of course, what I’m getting at are Black Swan events. These are rare and unpredictable events that significantly impact the economy. It was a concept introduced by Nassim Nicholas Taleb. Black Swan events include the Fall of the Berlin Wall, 9/11, the Global Financial Crisis and the Covid-19 global pandemic.

So, we have two ways to think about risk: one is the idea that it’s the likelihood of losing money, and the other is a measure of volatility. Or, to use a metaphor: one idea is the likelihood that the incoming tornado will kill you, and the other is how windy it’ll get. Knowing that the tornado might have winds above 140mph doesn’t tell you whether you should get out of Dodge. Relying on that historical information can often lead you completely astray.

Bear Sterns was doing great, right up until it was sold to JPMorgan for $10 a share (in the preceding year before the collapse, its share price peaked at over ten times that amount, at $133).

Equally important is the risk of bad events when the sun is shining. These are missed much more frequently.

The newspaper industry enjoyed relevance and sales until the internet absolutely destroyed their business model. Blackberry, the phone maker, was a safe bet, with solid sales figures until the iPhone came along and destroyed that market. Sony was the major player in consumer music until Apple introduced the iPod. Bookstores in the 1990s and even into the 2000s had solid sales figures before Amazon disrupted their business model. Amazon and Apple were also responsible for the fall of high street music retailers such as Virgin Megastores and HMV. Many of these businesses were at, or near, the peak just before the crash. Any historical risk measure based on a statistical analysis of historical returns or sales would have failed to spot this competitive risk. Even the people supposed to be good at spotting this risk didn’t. Private equity business Permira bid for HMV in 2006, just before the business fell off a cliff, resulting in administration in 2013.

Sony is a particular case to pull out. By all accounts, Sony should have been the company that built the iPod; after all, they had owned this industry since the introduction of the Walkman. Sony had the consumer electronics know how, the hardware design and production capabilities, and they had the relationships with the music companies. But they didn’t introduce the iPod.

In each and every one of these cases, the risk of fatal outcomes would have been deemed lower than it was. I acknowledge that this argument is somewhat circular. Those businesses that do understand risk would act before the event and change business model or product range, and we’d never read about it in the history books.

In finance, we saw bad events under-estimated based on historical data, and in the examples above, we saw bad events as being nearly nonexistent based on historical data.

The risk for financial companies came from new financial products like credit default swaps and collateralised debt obligations and the contagion they brought to the industry, plus the misunderstanding of the correlation between financial products (and a fair dose of near criminal activity, too). In the other examples, the risk came from technological and business model disruption.

In the second set of examples, the risk arose from being risk averse. The consequence of relying on the bell curve to measure possible risk is undoubtedly risk aversion because it’s not telling you where the next economic Black Swan event is coming from.

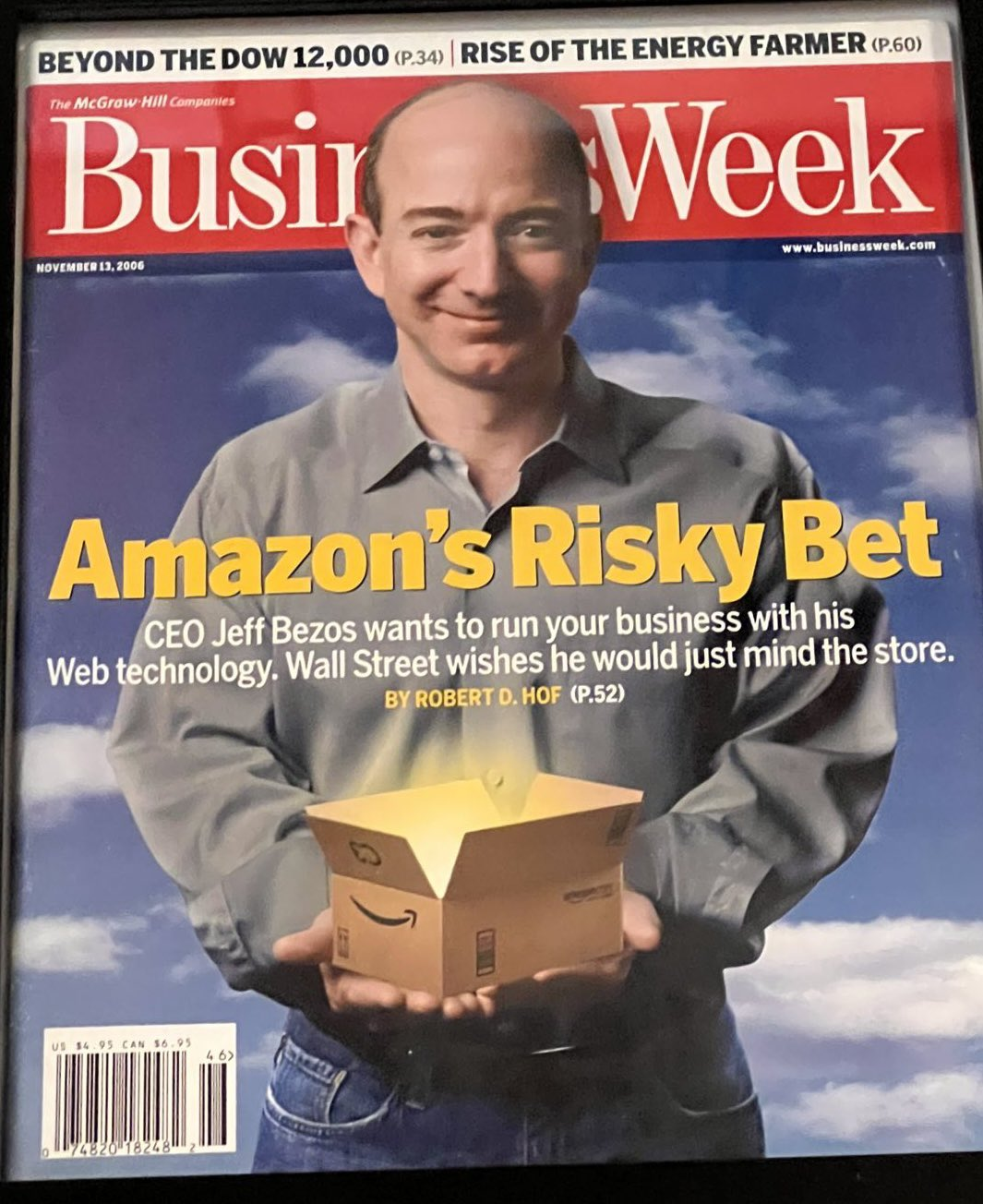

Risk aversion brings the fallacy that you don’t need to cannibalise yourself and don’t need to know the next big thing. One of my favourite business stories of all time is BusinessWeek’s 2006 cover story: “Amazon’s Risky Bet: CEO Jeff Bezos wants to run your business with his Web technology. Wall Street wishes he would just mind the store.” Now, AWS accounts for about 75% of Amazon’s operating profit. So I guess Wall Street was wrong, huh? Yes, again. AWS wasn’t a risky bet. It was probably the safest business bet of the 21st century.

As Steve Jobs said, “If you don't cannibalise yourself, someone else will”. He understood that risk didn’t come from looking to the past but instead from looking forward, and the risk was greater in not doing something and not building something new. (Of course, you can enact barriers to entry, eliminate competition and lobby the government to put in place anti-competitive regulation and legislation, which means no one else will cannibalise you, and then you don’t have to cannibalise yourself, but this is a bad outcome for everyone). Steve Jobs realised that if he didn’t kill the iPod and build capability within the iPhone, Samsung, Google, HTC and others at the time would kill the iPod for him. There is nearly always more risk in not doing something, than doing something.

It’s very easy, in large companies, to become risk averse and focus on small (pointless) incremental improvements, which you fool you into thinking they will reduce risk. All the while, a Black Swan is looking behind you. Google did not really move on AI until OpenAI did. Car manufacturers did not really develop EVs until Tesla and BYD did. The record companies did not embrace the internet and streaming business models until Napster and then Spotify came along. Longshoremen and their unions did not modernise until the shipping container forced them to.

There will always be cost-benefit analysis (one of the worst things ever invented) and risk analysis, which can quantify why you shouldn’t do something: why you shouldn’t enter the market, or why you shouldn’t introduce a new product, or that the new innovation is too small, or that the ROI isn’t worth it. The same is true for the economy, too: there’ll always be historical data that tells officials that the government is too indebted to build the new railway or invest in EV charging. What happens with cost-benefit analysis is that we overweight occurrences whose impact is small but whose outcomes we can immediately see (cost). We underweight occurrences whose impact is potentially huge, but the impact we cannot see (benefit). We’re risk averse because we base our measure of risk on what has historically happened. It’s a delusion. Nobody had jumped from space until Felix Baumgartner did it. The past is a good measure of the laws of physics. The past is a good measure of the laws of economics. But the past is a poor measure of risk.

A little less risk aversion, a little more action, please.

Reply